Credit Information

BlueNord actively manages its capital structure to support long-term value creation. A conservative balance sheet, disciplined use of debt, and proactive refinancing are central to how the Company underpins its operational strategy and its commitment to delivering material shareholder returns.

Our Approach to Capital Management

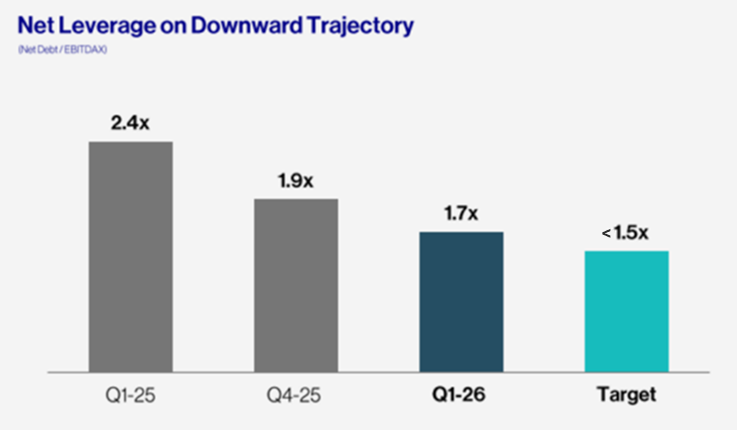

- Maintain a conservative balance sheet. Net leverage is targeted at approximately 1.5x, providing resilience through commodity price cycles and preserving the Company’s ability to sustain distributions.

- Proactive refinancing. BlueNord refinances instruments ahead of maturity, as demonstrated by the early redemption of BNOR15 in July 2025, the early redemption of BNOR16 in May 2026, and the two-year extension of the RBL in February 2026.

- Reflect business strength in bond terms. Each successive bond issuance has reflected the improved financial position of the Company – from the 9.5% coupon on BNOR16 in June 2024 to the 7.875% coupon on BNOR18 in May 2026.

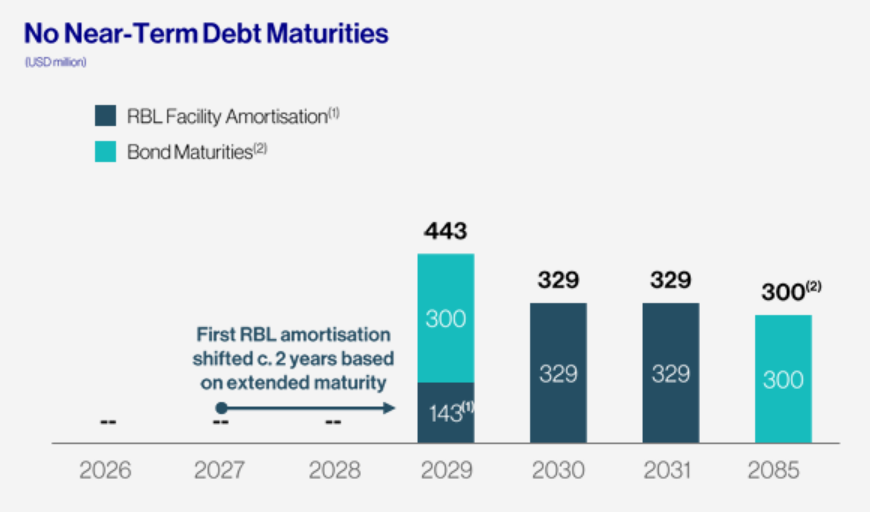

- No near-term debt maturities. Following the BNOR18 issuance and RBL extension, the Company’s next material debt maturity is the BNOR18 bond in 2031, with the first RBL amortisation not due until 31 December 2028.

Debt Maturity Profile

Net Leverage

Latest Transaction: BNOR18 (May 2026)

On 6 May 2026, BlueNord successfully placed a new USD 400 million five-year senior unsecured bond – BNOR18 – with maturity in 2031. The bond carries a fixed interest rate of 7.875% per annum and will be listed on Euronext Oslo Børs.

The issuance attracted strong demand from international and Nordic investors and was upsized from an initial target of USD 350 million to USD 400 million, with the book multiple times covered at final pricing. Settlement is expected on or about 19 May 2026.

The net proceeds are being used to redeem the Company’s existing BNOR16 bonds in full, for a partial repayment of the Reserve Based Lending (RBL) facility, and for general corporate purposes. The BNOR16 redemption at the prevailing make-whole call price takes effect on 22 May 2026.

The improved coupon – 7.875% on BNOR18 versus 9.5% on BNOR16 – reflects the strengthened financial profile of the business and provides greater long-term flexibility as BlueNord continues to deleverage.

“The successful placement of BNOR18 demonstrates continued confidence in BlueNord’s business, cash flow profile and long-term strategy. Strong demand throughout the marketing process allowed us to upsize the bond and secure attractive pricing. The new bond terms also provides greater long-term flexibility to support our business as we continue to deleverage and maintain a conservative balance sheet. This refinancing is fully aligned with our strategy of proactively managing the capital structure to support long-term value creation for all stakeholders.”

Jacqueline Lindmark Boye, Chief Financial Officer, 6 May 2026

BNOR17 Hybrid Bond

BlueNord successfully placed a new USD 300 million subordinated callable hybrid bond issue with maturity in 2085. The hybrid bond will have the first call at 100% of nominal value and coupon step up after 4.5 years. The new bond will carry a fixed interest rate of 12% per annum, payable semi-annually in arrears.

Net proceeds from the bond issue were used to refinance the Company’s subordinated convertible bonds with ISIN NO 0012780867 (“BNOR15”) in full.

“The successful placement of a hybrid bond marks a key milestone in the evolution of BlueNord’s capital structure. This instrument allowed us to refinance the convertible bond raised during our entry into the DUC in 2019, while preserving our financial flexibility and removing the equity dilution associated with BNOR15’s mandatory conversion. With Tyra fully onstream, we have a robust outlook for both production and cash flow while maintaining a disciplined and resilient balance sheet. This is an important step forward for the Company, and we look forward to continuing to deliver for all our stakeholders,” said Euan Shirlaw, Chief Executive Officer of BlueNord.

Bond History

BlueNord has a track record of proactive and disciplined debt management, refinancing instruments as the business has grown and its financial profile has improved. The table below summarises the Company’s bond issuance history.

| Bond | Type | Amount | Coupon | Issued | Maturity | Status |

|---|---|---|---|---|---|---|

| BNOR15 | Subordinated convertible | ~$258m | 6.0% p.a. | Pre-2024 | – | Redeemed July 2025 |

| BNOR16 | Senior unsecured | $300m | 9.5% p.a. | 13 June 2024 | 2 July 2029 (original) | Redeemed 22 May 2026 |

| BNOR17 | Subordinated callable hybrid | $300m | 12.0% p.a. (steps to 17% after 4.5 yrs) | 10 July 2025 | 2085 (first call ~Jan 2030) | Outstanding |

| BNOR18 | Senior unsecured | $400m | 7.875% p.a. | 6 May 2026 | 2031 | Outstanding |

Reserve Based Lending Facility

In addition to its bond debt, BlueNord maintains a USD 1.4 billion Reserve Based Lending (RBL) facility, which provides the Company with significant financial flexibility. The facility is secured on a first-priority basis against certain of the Company’s subsidiaries and their assets, and constitutes senior debt in the capital structure.

In February 2026, BlueNord successfully closed an extension of the RBL maturity by two years. The key terms following the extension are set out below.

| Facility size | Drawn (Q1 2026) | Undrawn | Maturity / amortisation |

|---|---|---|---|

| $1.4 billion | $800 million – cash $200 million – letter of credit | $350 million | 31 Dec 2031; first amortisation 31 Dec 2028 |

The RBL contains a financial covenant requiring net debt to EBITDAX of less than 3.0x, tested on audited full-year financial statements, and a minimum liquidity covenant of USD 50 million on a forward-looking basis. At Q1 2026, net leverage stood at 1.7x, well within the covenant threshold.